A player decides to sign up. They go through registration, get to the deposit page, and their card gets declined. No explanation, no alternative offered. They close the tab.

That interaction cost the operator acquisition spend, a funded account, and, in most cases, that player permanently. And it happened entirely inside the payment flow.

Payments tend to be treated as operational infrastructure: something that needs to work, but not something that needs much strategic thought once it’s in place. That assumption is expensive. The payment experience is often the first real moment of friction between a platform and a player, and research from Fluid Payments puts the cost clearly: 27% of players leave a platform because of payment frustrations. Not because the games were bad. Not because of a weak promotion. Because a transaction failed or a withdrawal took too long.

That’s not a small issue. It’s a consistent leak that compounds across every market an operator works in.

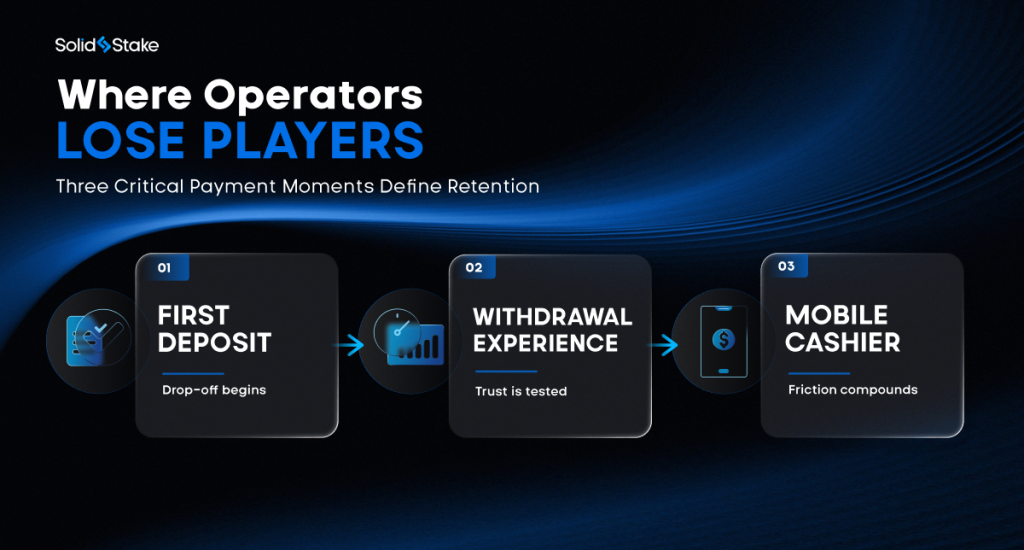

The first deposit is where things actually break

A lot of attention goes into sign-up conversion, getting someone to create an account. But registration without a completed first deposit means nothing commercially. The gap between someone who has signed up and someone who has actually played is where operators quietly lose a meaningful share of the traffic they paid to acquire.

The most common cause is a declined deposit. 52% of bettors have had a deposit declined on a betting app, and of those who encounter payment problems during sign-up, 17% don’t return at all. In a high-risk merchant category where card decline rates can exceed 30% in certain markets, this is a structural problem, not an occasional edge case.

The operators who handle this well tend to think about it differently. They treat multi-acquirer routing, fallback options, and alternative methods not as complexity to manage, but as a baseline requirement for keeping deposits alive. And the data on specific improvements is concrete:

- Showing locally preferred methods at the top of the cashier page can boost conversion by up to 80%

- Embedding payment flows in-page rather than redirecting players elsewhere delivers around a 30% conversion lift on its own

- Casinos that clearly communicate payout times and localised options see an average 21% conversion improvement

These aren’t exotic optimisations. They’re well-understood improvements that a lot of operators simply haven’t made a priority.

Local payment methods aren't a nice-to-have

iGaming is a global industry, but how people pay is intensely local. Players don’t adapt their payment habits to fit a platform, they expect the platform to fit them.

In Europe, bank-based methods like Trustly and iDEAL have become standard. In Brazil, PIX has essentially taken over, gambling-related PIX transactions grew by 200% from January 2024, and the method is used by more than 70% of the country’s population. Across Southeast Asia, wallets like GrabPay and Alipay are the default. Globally, digital wallets already account for roughly half of all online spend.

Local payment methods function as a trust signal before a single game is played. Players see a familiar method and feel like they’re on a platform built for them. They see something unfamiliar, and they look for one that was. Optimising payment coverage for a specific market can lift deposit conversions by 20 to 40%, particularly in high-growth regions. For operators planning expansion, this isn’t a phase-two consideration, it belongs in the market-entry decision.

What the cashier page signals before a player deposits

A player from the Netherlands who sees iDEAL at the top of the cashier page gets a clear message: this platform understands my market. A player in Brazil who finds only cards gets a different one: this wasn’t really built for me.

That’s not just perception. Transparency about how payments work ( what methods are available, what fees apply, how long withdrawals take) directly shapes conversion. Players don’t necessarily need everything to be instant. They need to know what to expect. A withdrawal that takes 24 hours is usually fine. One that disappears into a queue with no communication erodes trust in a way that’s difficult to recover from.

Operators who treat the cashier with the same care they give to the game lobby (the copy, the layout, what gets shown first) consistently see different results. It’s not just a form. It’s a surface that reflects the quality of what’s behind it.

Withdrawals: the retention lever most operators underuse

Deposits get the focus. Withdrawals drive retention.

There’s a consistent pattern in how operators approach the payment lifecycle: considerable thought goes into the deposit funnel, and withdrawal processing gets left to whatever the payment provider’s defaults happen to be. It’s understandable, deposits generate revenue, withdrawals don’t. But that framing misses something important.

67% of players identify fast withdrawals as a top loyalty driver. Instant withdrawals can improve retention by around 30%. And the UK Gambling Commission, which handles more than 2,000 withdrawal complaints per year, has identified a clear pattern in its enforcement data: operators with easy deposits and difficult withdrawals. That asymmetry is one of the more reliable ways to damage long-term trust.

It’s also worth noting who feels this most acutely. High-value players, the ones contributing the most to GGR (Gross Gaming Revenue) have lower tolerance for friction and more alternatives available. When a withdrawal experience disappoints them, they rarely complain. They move somewhere else.

Real-time payment rails make fast withdrawals operationally achievable for operators who build around them. The infrastructure exists. The question is whether it’s been treated as a priority.

Mobile is where a lot of conversion is being lost quietly

71.7% of all online gambling now happens on mobile. These numbers have been moving in the same direction for years.

And yet many operators still run payment flows designed for desktop, with mobile as an adaptation rather than the starting point. On mobile, redirects and multi-step processes create friction at exactly the wrong moment, when a player has decided to deposit and just needs to complete it. A distraction, a slow load, an unfamiliar form layout, and the moment passes.

Adding Apple Pay and Google Pay to a mobile-first cashier has been shown to reduce deposit friction by 40%. One-tap options convert better for a straightforward reason: they collapse the distance between intent and action.

A cashier that looks fine in a product review can quietly lose deposits in production, not because the product is bad, but because the flow wasn’t designed for how people actually arrive at it.

Compliance doesn't have to break the deposit experience

Every regulated market brings KYC requirements, AML checks, and transaction monitoring. That’s not changing. What varies significantly between operators is how those requirements are implemented, and how much friction they create in the process.

A verification request that interrupts a first deposit, with no explanation of why it’s needed or what comes next, drives abandonment. The same requirement, integrated into a well-designed onboarding flow with clear communication, converts at a meaningfully higher rate. The compliance obligation is identical. The outcome is different.

Fraud in online gaming grew by 64% between 2022 and 2024, so the compliance burden is real and increasing. But there’s more room than most operators use between a compliant experience and a punishing one. Passport scanning with field auto-population, stepped verification that doesn’t front-load all the friction at the cashier, clear messaging about what’s required and why. These are design decisions with direct conversion implications.

Payment data and CRM: a connection most operators haven't fully made

For operators who have built CRM as a core retention function, payment data is one of the most useful signals available and one of the most underused.

Deposit frequency, preferred methods, withdrawal timing, shifts in transaction patterns: all of these carry real information about how engaged a player is and where they might be drifting. Operators who connect payment signals to their CRM can act on that earlier, matching offers to how someone actually pays, or identifying a change in deposit behaviour before it shows up in gameplay data.

The catch is that fragmented payment infrastructure makes this difficult. Multiple providers with inconsistent data formats, settlement timelines that vary by method, no unified view of a player’s payment history. These gaps leave the retention team working with an incomplete picture of the players they’re trying to keep.

The architecture question isn’t just which payment methods to support. It’s how the payment layer integrates with the rest of the operational stack, and whether the data it generates is actually usable downstream.

Treating payments as a strategic function

The operators gaining ground have stopped treating payments as a cost-centre problem and started treating them as a strategic one.

The evidence is consistent. Reducing deposit friction improves funded accounts. Localising payment methods lifts conversion in new markets. Fast withdrawals retain the players worth retaining. Connecting payment data to CRM produces better retention outcomes. None of this is new information, most operators know the gap exists.

What separates the ones who close it is whether payments receive the same deliberateness as product and marketing, or whether they’re still being handled like infrastructure that just needs to run.

The cashier is often the first real interaction a player has with a platform. It’s worth building it that way.